What is a Credit Score? How It’s Calculated and Why It Matters for Your Future

In the modern financial ecosystem of 2026, your credit score is more than just a number; it is your “financial reputation” distilled into a three-digit figure. Whether you are looking to rent a high-end apartment, buy your first electric vehicle, or secure a mortgage for a family home, your credit score will be the first thing lenders look at.

Understanding how this score is built and maintained is one of the most significant steps you can take toward long-term financial freedom. This comprehensive guide will break down the mechanics of credit scores, how they are calculated in the current market, and why they are the key to your future wealth.

What is a Credit Score?

A credit score is a statistical number used by lenders to evaluate the risk associated with lending money to a consumer. It predicts the likelihood that you will pay back a loan on time. In the United States and many other global markets, the most commonly used models are FICO® and VantageScore.

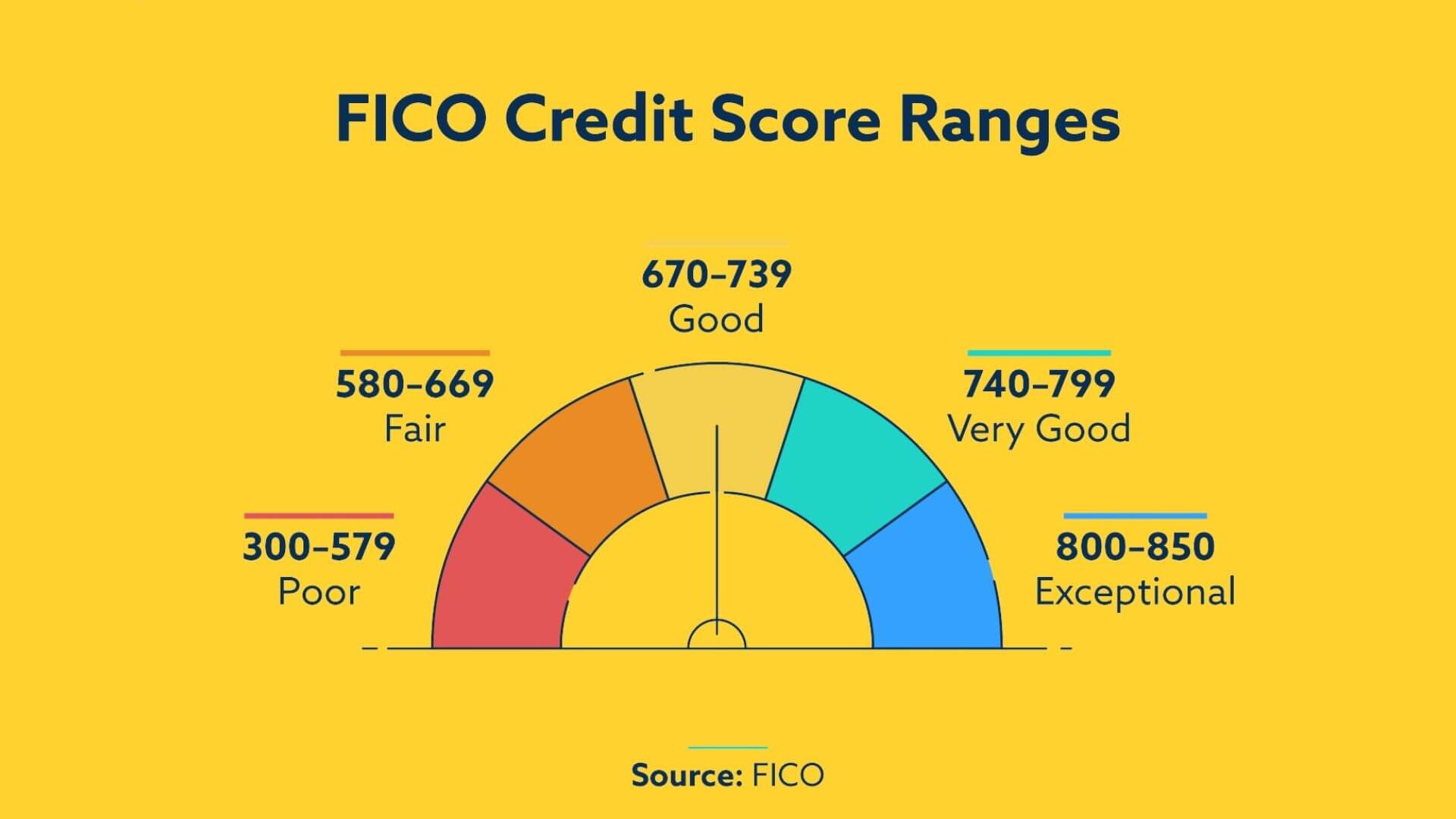

Credit scores typically range from 300 to 850:

-

300–579: Poor

-

580–669: Fair

-

670–739: Good

-

740–799: Very Good

-

800–850: Exceptional

How Your Credit Score is Calculated (The FICO Model)

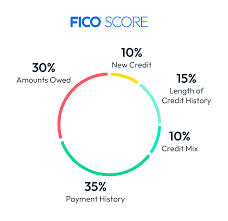

While the exact algorithms are proprietary, the FICO model—which is used by 90% of top lenders—breaks down your score into five distinct categories. Understanding these percentages allows you to prioritize your financial habits.

1. Payment History (35%)

This is the most critical factor. Lenders want to know if you pay your bills on time. Even a single payment that is 30 days late can cause a significant drop in your score. Consistent, on-time payments over years build the strongest foundation.

2. Amounts Owed / Credit Utilization (30%)

This is the ratio of your outstanding debt to your total credit limits. For example, if you have a credit card with a $10,000 limit and you owe $3,000, your utilization is 30%. Financial experts recommend keeping this under 30%, though those with the highest scores often keep it under 10%.

3. Length of Credit History (15%)

The longer you have held credit accounts, the more “predictable” you are to a lender. This is why it is often a mistake to close your oldest credit card account, even if you don’t use it frequently; doing so shortens your average account age.

4. Credit Mix (10%)

Lenders like to see that you can handle different types of debt. A healthy “mix” might include “revolving” credit (credit cards) and “installment” loans (student loans, auto loans, or a mortgage).

5. New Credit (10%)

Opening several new credit accounts in a short period represents a higher risk, especially for people who do not have a long credit history. Each time you apply for credit, a “hard inquiry” is performed, which can temporarily dip your score.

Why Your Credit Score Matters for Your Future

Many people mistakenly believe a credit score only matters when they want to borrow money. In reality, your score affects almost every aspect of your adult life.

1. Interest Rates and Total Cost of Debt

The difference between a “Fair” score and an “Exceptional” score can cost you hundreds of thousands of dollars over a lifetime. A higher score qualifies you for lower interest rates. On a 30-year mortgage, a 1% difference in interest can mean the difference between an affordable monthly payment and financial struggle.

2. Approval for Rental Housing

In 2026, the rental market is more competitive than ever. Landlords frequently run credit checks to determine if a tenant is likely to pay rent on time. A low score might result in your application being rejected or being asked to pay a significantly higher security deposit.

3. Employment Opportunities

Some employers, particularly in the finance, government, or high-security sectors, perform credit checks as part of the background check process. They view a responsible credit history as an indicator of general organizational skills and reliability.

4. Insurance Premiums

In many regions, auto and homeowners insurance companies use “credit-based insurance scores” to help determine your premiums. Statistically, individuals with higher credit scores tend to file fewer claims, leading to lower monthly insurance costs.

5. Utility Deposits

When you move into a new home, utility companies (electricity, water, internet) check your credit. If your score is low, they may require a substantial upfront deposit before activating your services.

How to Improve Your Credit Score in 2026

Improving your score isn’t an overnight process, but by following these steps, you can see significant movement within 6 to 12 months.

Step 1: Check Your Credit Report for Errors

Under the law, you are entitled to a free credit report from each of the three major bureaus (Equifax, Experian, and TransUnion). Check these for accounts you didn’t open or late payments that were actually made on time. Disputing these errors is the fastest way to boost a score.

Step 2: Automate Your Payments

Since payment history is 35% of your score, you cannot afford a mistake. Set up “Auto-Pay” for at least the minimum balance on every account to ensure you never miss a deadline.

Step 3: Pay Down Balances to Lower Utilization

If you have a “maxed out” credit card, your score is being suppressed. Focus your extra cash on paying these balances down to below 30% of the limit. You will often see a score increase as soon as the bank reports the new, lower balance to the bureaus.

Step 4: Become an Authorized User

If you have a thin credit file, a family member with excellent credit can add you as an “authorized user” on their oldest card. You don’t even need to use the card; their long history and high limit will be reflected on your report.

Conclusion: Take Control of Your Financial Identity

Your credit score is a tool. When managed correctly, it opens doors to lower costs, better housing, and greater financial flexibility. In the economy of 2026, being “credit-literate” is a superpower. By paying your bills on time and keeping your debts low, you aren’t just pleasing a bank—you are investing in your own future